Working out what can be claimed as travel deductions is an area many taxpayers find confusing.

To obtain a deduction three “golden rules” need to be considered and met:

- the expense must be spent, and not been reimbursed;

- it must be work related; and

- you must be able to substantiate the expenditure.

The most common question we get asked – “is my home to work travel claimable?” Firstly, home to work travel is generally considered private

in nature and no deduction would be available in this instance.

There are, however, circumstances where trips between home and work can be claimed, if the travel is considered to be related to gaining or

producing assessable income, rather than simply “getting to” a place to start work.

Deductible Travel Expenses

Travel can be claimed from home, and work, provided that:

- The nature of your work is itinerant and when you travel between two separate places of employment (not home);

- You are required to carry bulky tools or equipment and there is no secure place available at the workplace to store them.

- You are “on call” and work is regarded as having commenced before leaving home.

- You are working on multiple sites and travelling between those sites.

- Home is your base of employment and you are required to start the work at home and travel to a workplace to continue the work.

- You travel between home and an alternative workplace and stay overnight (paid to travel).

-

Travel is undertaken in response to a business-related emergency call from home to work which does not follow normal daily routines. This

does not extend to an individual who chooses to work at home.

- You are using your car to see your tax agent for the preparation of tax returns and other business-related matters.

Self-Education

As a general rule, the cost of travel for self-education is claimable provided the essential connection to the earning of assessable income

can be established, and it is directly related to your current employment. For example, if you travel from work, to your place of education,

this travel would be deductible, and vice-versa.

Non-deductible Travel Expenses

Travel is private in nature if:

-

It relates to minor work-related tasks performed between home and work. For example, incidental tasks performed on your way to work or home

such as picking up the mail.

-

Work is performed outside ordinary hours, such as shift work or overtime, or by someone who is on call or stand-by, where work only

commences on arrival at the workplace.

- Moving to a new location of employment or use of public transport to attend work.

- Traveling to an alternative workplace, where you are not required to stay overnight (not paid to travel)

- Work is performed at home which does not constitute the performance of substantial employment duties.

From 1 July 2017, travel expenses incurred for residential investment properties relating to inspecting, maintaining or

collecting rent is not deductible.

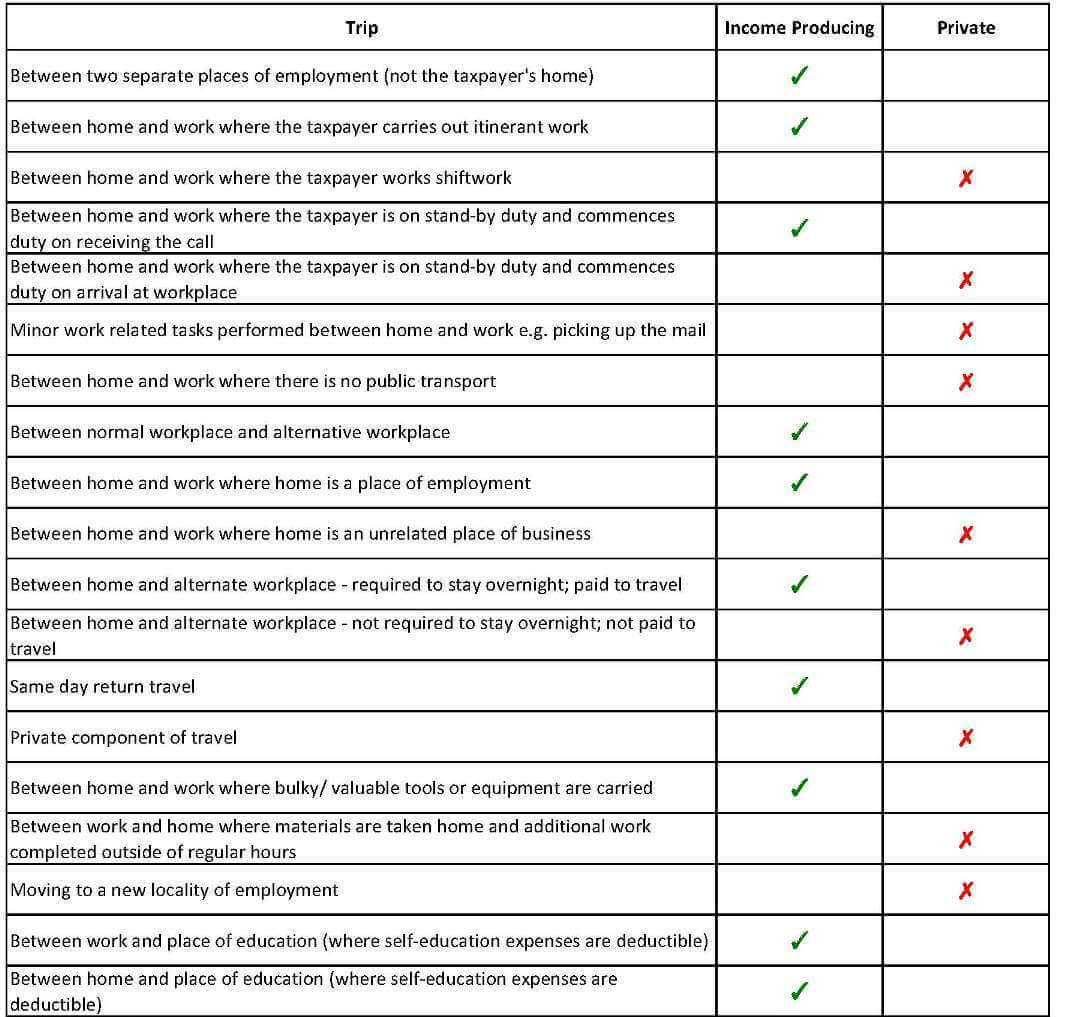

Summarised below is a table of various scenarios which we all encounter:

Source: Tax Banter, 2018

Please note the information in this article is general in nature and may not necessarily be appropriate for your circumstances. If you wish

to discuss, please contact Ashfords.