What’s this new tax:

On 20 March 2024, the Victorian State Government introduced the Commercial

and Industrial Property Tax Reform Bill 2024 (legislation.vic.gov.au).

The Bill is expected to become law and to take effect from 1 July 2024.

The Victorian Government, as announced in the 2023-24 Budget, is progressively abolishing stamp duty on commercial and industrial

property and replacing it with an annual tax.

The annual tax, to be known as the Commercial and Industrial Property Tax (CIPT), will be set at 1% of the

property’s unimproved land value.

The tax will replace land transfer duty (stamp duty) that is currently payable on the improved value of the land when you purchase or

acquire a commercial or industrial property in Victoria.

The new tax system will start to apply to commercial and industrial property if the property is transacted on or after 1 July 2024.

How will it work:

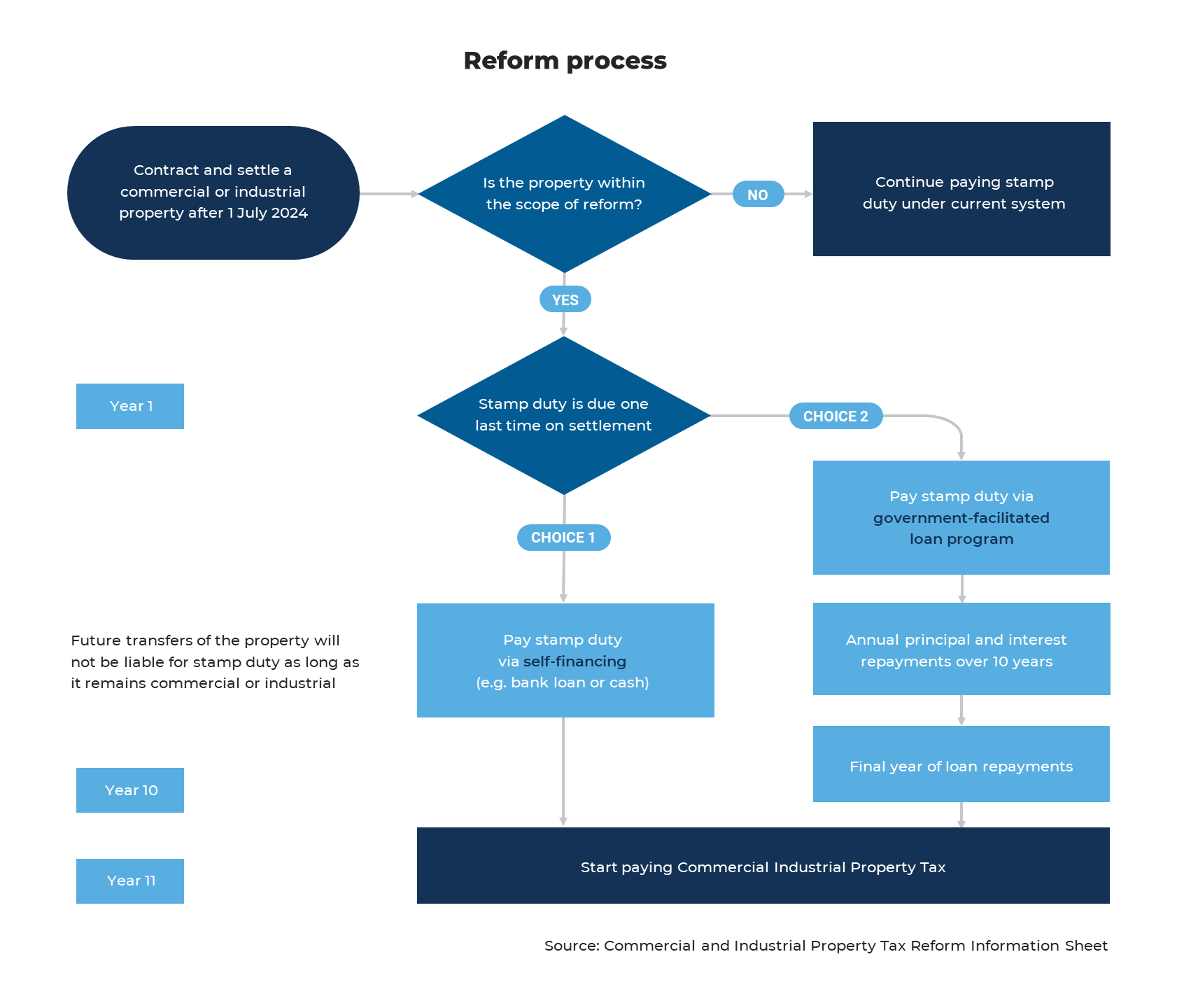

A commercial or industrial property will enter the CIPT regime if:

- a contract of sale for the property is entered on or after 1 July 2024;

- 50 per cent or more of the property transacts;

-

stamp duty is payable on the transaction (ie the transaction is not exempt from stamp duty);

and the property has a qualifying commercial or industrial use at the date of settlement.

If a property enters the CIPT regime:

-

the normal rate of stamp duty will be payable on the transaction that causes the property to enter the CIPT regime. However, to ease

the transition to the new tax system, the Government will give the purchaser the option of accessing a government-facilitated transition

loan as an alternative to self-financing the upfront stamp duty amount;

-

stamp duty will not be payable on any future transactions involving the property, for as long as the property continues to have a

qualifying commercial or industrial use; and

-

CIPT will be payable annually commencing 10 years after the property enters the CIPT regime by whoever owns the property on 31 December of

the relevant year. It will be payable for as long as the property continues to have a qualifying commercial or industrial use.

The CIPT regime will not apply to properties primarily used for residential purposes, community services or sport, heritage and culture

purposes.

Overview:

The Commercial and Industrial Property Tax is a replacement for stamp duty, and is separate to land tax, which will continue to apply. This

reform does not make any changes to existing land tax arrangements.

For commercial and industrial property that is transacted on or after 1 July 2024 and enters the new tax system, landowners will start

paying the Commercial and Industrial Property Tax 10 years after the initial transaction. However, stamp duty will not be payable on

transactions involving the property that take place after the property enters the new tax system.

To discuss how these changes may impact you, please contact your Ashfords Manager or Partner, on 03 9551 2822.